When looking at the shape of the yield curve it’s easy to see that a lot has changed. Low yields overall have certainly pinched bond investors and made them look elsewhere for returns, but not all investors are so flexible. For banks who are restricted in terms of the investments that they are allowed to hold, the decision of where in the bond market to invest is an important one as well.

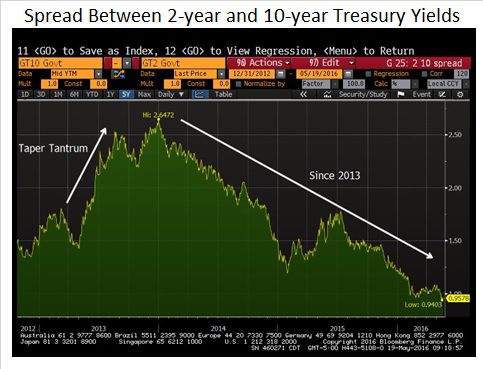

One way to interpret the graph above is that since 2013, longer duration bonds have gotten a lot less attractive. While short term interest rates have been more or less pegged at zero, longer-term interest rates have fallen dramatically since the aftermath of the taper tantrum in the middle of 2013. After peaking in late 2013 at a yield over 3% the ten-year treasury yield has fallen to 1.80% despite the Fed cutting back on their buying activity in that part of the market. So what was the catalyst for this large move?

Looking back at the market’s expectations in 2013, the consensus was that interest rates would more or less be normalized by now. That meant fed funds somewhere between 2% and 3% and the ten-year yield over 4%. Instead we got one small Fed Funds hike at the last meeting of 2015 and every spot on the yield curve longer than 1-year has fallen. Economic growth has been disappointing, inflation has failed to return to the long run average and economic issues overseas have caused massive appreciation in the value of the dollar. All these factors have put further pressure on yields and delayed the expected path of Fed action.

While there has been very little change in the factors that impact longer-term yields, the FOMC is again signaling their intention to raise short-term rates. Minutes from the April meeting that were released yesterday signal much more willingness to raise short-term rates again – putting further pressure on investors that make a living on a steep yield curve.

So what is a bank to do?

First of all consider the risks. If pushing out the duration of your investment portfolio didn’t make sense in 2013, it certainly doesn’t make sense now. The risk is the same, the only thing that changed is your compensation for taking the risk. For those who did take some additional duration risk, congratulations. You were paid well, but you probably have new cash to invest. The curve is still positively sloped, so there is some additional return to be had for stepping out, but you’re right to be less enthusiastic about the strategy. You’re probably okay doing some, but you shouldn’t assume the same result as before.

On the flip side. Perhaps revisiting your funding strategy would be beneficial. If you accept that taking additional duration risk is less attractive, then funding your balance sheet with longer duration term deposits is more attractive. Consider, of course, the impact on profitability, but it could be a great opportunity to diversify your funding profile and hedge the bank on an asset liability basis.

Regardless of your view on the next 12 months, the environment is different, and because of that, your strategy should change with the times.