Despite the frenetic trading in the markets yesterday, I was heartened as I talked and emailed with clients who seemed largely unfazed by the steep selloff over the last week.

Not only was no one panicking, a handful of clients (not just mine, but for the firm), sent in new money to capitalize on lower prices while a number simply wanted to rebalance their existing assets, which at this point means selling some bonds and buying more stocks.

I did my duty and said that stocks may go lower from here, which is something everyone knew before I said anything. I told them that I had added to my own emerging markets exposure thinking that it was a good deal on Wednesday, only to find out that it would have been a much better deal yesterday and everyone knows that my parable applied to their fresh deposits as well.

What’s so encouraging is that the people that I talked to really do have the right long-term time horizon in mind as part of an overall financial plan. Of course, no one likes the losses and recognizes that there may be more in the coming days, but I think everyone also understands that stocks make good investments over the long run.

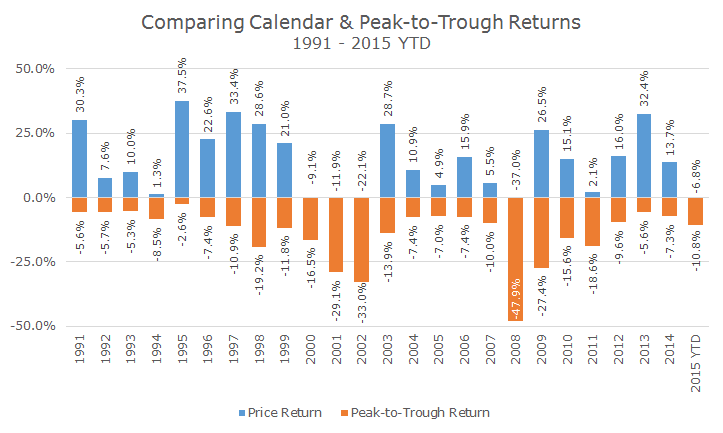

You know I can’t help myself when it comes to charts, so I thought I would include a relatively straightforward snapshot that compares the annual calendar return for the S&P 500 along with the worst performance drawdown in that same year.

So, for example, in 1991, the first year for the chart, the S&P 500 index gained 30.3 percent. Within 1991, however, the index fell -5.6 percent over just a few days in November. In some years, like 2002, the peak-to-trough loss was much worse than the calendar year loss.

The point here, though, is that it’s common to lose from one point to another within the course of a year. During this 25-year period (okay, 24.75 year) the average peak-to-trough loss is -13.8 percent. That period contains two terrible markets, so if you look at the median peak-to-trough loss instead, it’s -10.0 percent. In other words, the rout that we’re going through, while more swift than usual, is typical so far.

A simple buy and hold strategy that endured all of the ups and downs for the market would have earned 9.4 percent per year over that time period, just a hare under the long-term average despite two of the five worst bear markets in history, which I find remarkable.

You have to remember too that if stocks weren’t risky, they wouldn’t earn anything either. We all know that cash has almost no loss of principal, but the returns are paltry and didn’t even keep up with inflation when they yielded something more than zero.

It’s easy to get swept up in the media frenzy when things are sour and I like what one of my clients did when he turned on the TV and saw what was happening: he turned it right off and went back to his daily business. We’ll take care of the rebalancing or tax loss harvesting, if appropriate, and you can take a walk and enjoy the unseasonably cool August that we’re having.