During the 2008 financial crisis, the Federal Reserved used a variety of tactics to stabilize the economy and financial system. First they cut interest rates, but when they got to zero and couldn’t cut anymore, they started buying bonds in the open market in a process call quantitative easing (QE).

The program was controversial because a lot of people thought that it would stoke inflation. While that didn’t come to pass, it’s still a hot issue because the Fed still owns those bonds and the process of unwinding those purchases could be painful.

The issue has been quiet in recent years because the Fed stopped buying bonds (other than reinvesting interest payments and maturities), but comments related to the last meeting brought the issue back to the forefront.

When the Fed bought bonds, they created cash out of thin air. If they had used their own cash, their balance sheet would have stayed the same since the cash would have declined by the same amount as the bonds that they purchased.

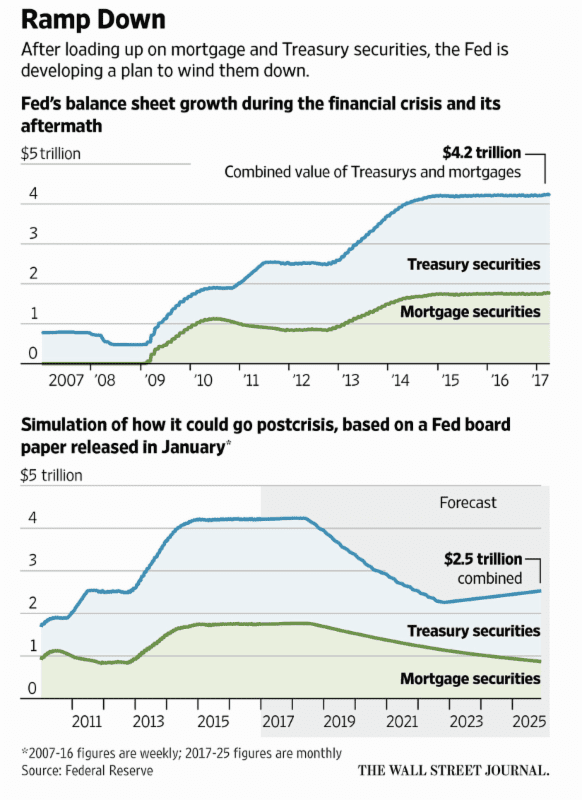

Instead, their balance sheet exploded, which you can see in the charts below from the Wall Street Journal (you can find the article here, but it may require a subscription). The numbers are staggering – you can see that the balance sheet was less than $1 trillion before the crisis and now stands well over $4 trillion.

The second chart shows how the Fed thinks the balance sheet could shrink in the coming years if Fed stops reinvesting the interest payments and maturities. Notice that even after it shrinks, their balance sheet still stands around $2.5 trillion – much more than the $1 trillion they had 10 years ago.

To some extent, the idea that the Fed is talking about shrinking their balance sheet is good news because it means that they think that the economy is in good enough shape to absorb the stimulus withdrawal (to be sure, it’s partly politics because Chair Yellen wants to start the process while she’s still got a job).

What does a shrinking balance sheet mean for us? It’s hard to say, but the immediate concern is that the process could send interest rates higher, which would hurt bond prices in the short run.

Why would rates go higher if the Fed shrinks their balance sheet? For the same reason that QE lowered rates. When they were buying, they created demand, which probably pushed prices up, which lowered yields. In theory, the absence of the Fed and their buying could lower prices, which would push up yields.

Personally, I’m not so sure. I’m not an economist by any stretch, but it seems to me that letting the bonds mature isn’t the same thing as selling them, which would put downward pressure on prices in my opinion.

At the same time, I don’t trust the predictions on the matter – keep in mind that a lot of reasonable, smart people thought that QE would lead to high inflation, which didn’t come to pass. Predictions are a tough business.

In my mind, it was a huge experiment and it’s tough to say how it will go from here. Personally, I am happy to have the government reducing their influence on the market, even though I’m unsure about what will happen next.