I’m amazed that the year-to-date return for all of the non-US stocks are up 26.2 percent, and the S&P 500 is ‘only’ up 15.7 percent.

It seems like a long time since global stocks have outperformed the S&P 500, so I decided to do some digging. I started with a slightly different index than what I use in the market summary. The summary is all non-US stocks, but for further analysis, I used the MSCI EAFE index, which is the longest running index of foreign stocks.

The MSCI EAFE is all of the developed markets like Germany and Japan, but excludes Canada, which seems like a funny exception. More importantly though, the EAFE doesn’t include emerging markets stocks like China, Brazil, etc., which have much shorter histories.

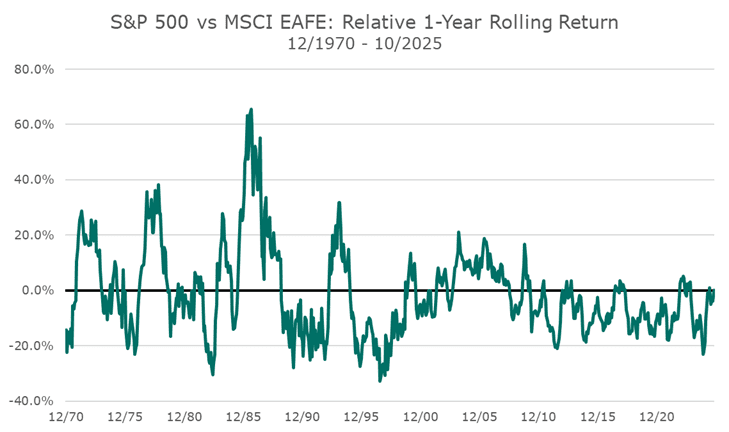

The chart below shows the rolling one-year performance differential between the S&P 500 and the MSCI EAFE. When the index is below the zero line, which is in bold, it means that the EAFE underperformed, and when it’s above the line, it outperformed.

My feeling that it feels like a long time since foreign stocks have outperformed is born out in this chart. Even the most recent 12-month rolling return that ends on October 31st, is barely positive.

Looking back at the entire time frame, we see that over the last 55 years, EAFE has meaningfully outperformed the S&P 500 in several distinct periods — most notably in the late 1980s and again from roughly 2003 through 2007, when we were a new firm.

Since the Global Financial Crisis, however, the experience has been almost the exact opposite: the United States has dominated for most of the last fifteen years, and the relative performance line has spent the vast majority of the time below zero.

What struck me when looking at the chart is how persistent these cycles can be. When one region leads, it often continues for years rather than months. The reversals tend to be sharp, and they often coincide with changing macro environments — interest-rate policy, currency cycles, commodity trends, or valuation extremes.

Given how long U.S. outperformance has lasted, it’s easy to forget that leadership alternates over time. The recent strength in international markets may or may not be the start of a new cycle, but it does reinforce an old lesson: global diversification can feel unrewarding for long stretches, right up until it is not. And when the cycle turns, it can turn quickly, as we see this year.

For us, the takeaway is not that we should suddenly shift dramatically toward international stocks, but rather that staying globally diversified remains as important as ever, especially given the relative valuations between the US and overseas markets.

We maintain exposure around the world not because every year rewards it, but because over time (albeit a potentially really long time), leadership rotates, opportunities arise in different places, and portfolios built to endure tend to benefit from multiple sources of return.

While not having the large US technology stocks has caused performance to lag for more than a decade, if those stocks are overvalued, including foreign stocks means less downside if investors have a change of heart on tech stocks.

It’s far too soon to draw any conclusions, but it’s still heartening to see foreign stocks working so well this year after a long stretch of underperformance.