Over the last six months or so, small-cap stocks have enjoyed one of their strongest periods of relative performance in history.

In the five months that ended in February, the S&P 500 is up 14.1 percent, which is a terrific return, but the S&P 600 Small-Cap index, is up 50.3 percent, which is tremendous. This month isn’t over, so it’s too soon to say for sure, but as of Friday, the S&P 600 Small-Cap index is up another 9.4 percent, while the S&P 500 is up 3.6 percent.

Large-cap stocks started crushing small-cap stocks in January 2017 even before the pandemic started, as the S&P 500 grew 53.1 percent, while small-caps ‘only’ made 22.2 percent. The pandemic exacerbated the performance differential when over the next eight months (February through September), large-cap stocks made 5.6 percent while small cap stocks lost -11.7 percent.

Even if you aren’t following all of the ups and downs, the long and the short of it is that large-cap stocks were substantially better than small-cap for several years before the pandemic and the pandemic made the margin even higher. Maybe some charts will help illustrate the point.

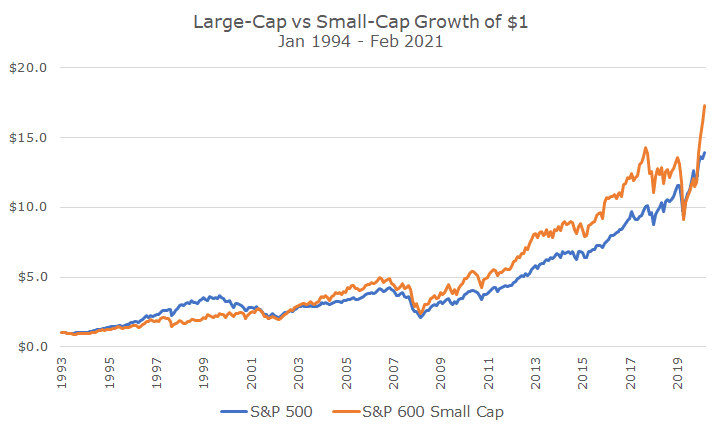

The first chart shows the growth of $1 invested in both the S&P 500 index of large-cap stocks and the S&P 600 index of small-cap stocks:

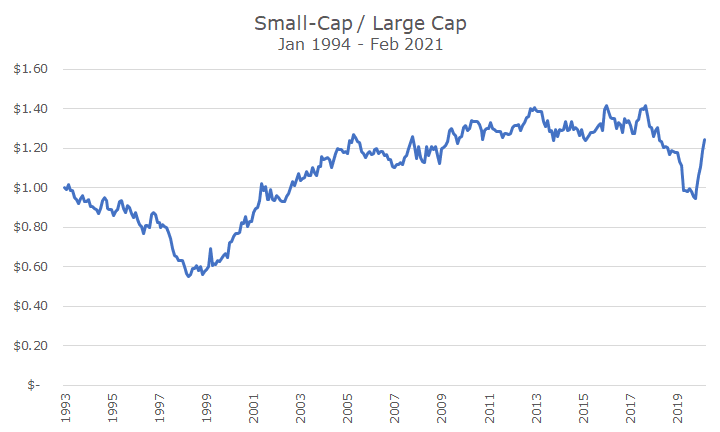

This second chart shows essentially the same thing, but strips out the growth of the overall market, and just shows the relative performance of small-caps over small-caps.

Here you can see that in the late 1990s, during the tech-bubble, large-cap stocks materially outperformed small-cap stocks. When the bubble burst, small-caps started to outperform dramatically until the real-estate bubble and was modest until 2017 when the game changed again.

And, as good as it’s been in the last five months, small-caps haven’t fully recovered all of their outperformance relative to large-caps.

If the rally this month holds (and that’s a BIG if, since we’re only halfway through the month), almost all of the underperformance of the last few years will be erased.

And that’s the point of this article: it would have been impossible to know six months ago that a years-long period of material under-performance could erase itself in such a short time.

Over the past few years, I’ve been asked what feels like a million times whether small-cap stocks could ever come back. I never had a great answer, which amounted to something like, ‘I hope it does.’

I couldn’t have said, ‘Well, for this to come back, what we’re going to need is a global pandemic that will cause the government to create trillions of dollars of stimulus…’

And if you ask me today whether the rally will continue, or will things will go from here, I’ll offer the same sheepish smile and try and sound smart while saying I don’t know (it’s a tricky balance!).

What I did say, and will continue to say, is that small-cap stocks have historically outperformed large-cap stocks. That makes sense to me since they are riskier than large-cap stocks, and riskier investments should have higher returns to compensate for that risk.

That doesn’t always work, even in small caps. There are long-stretches (very long stretches) where large-cap stocks fare better than small-caps.

But since we can’t predict when how long those periods will be or what will serve as a catalyst for change, we’ll just keep holding our strategic long-term weights, trying to hold on during the bad times, and enjoying the good times.

And, in both instances, we will rebalance: reducing small caps when they rally, and adding to them when large-cap rallies.

For now, though, these are the good times, so enjoy!

David is a trusted advisor to 50 families, delivering comprehensive financial solutions, including financial planning, investment management, cash management, tax planning, estate planning, and charitable giving. As Chief Investment Officer, he leads the Investment Committee and the research and trading team. His team continuously evaluates investment strategies and securities, working closely with Portfolio Managers to implement them effectively.