Every day brings another headline (or Presidential tweet) about escalating trade tensions between the US and the rest of the world. What impact could these tariffs have on the bond market?

The most popular narrative is that prices may increase due to tariffs being passed through to US consumers. Higher inflation should lead to higher long-term rates and the potential of a more hawkish Fed. This “cost-push” view of inflation is great in a textbook, but rarely happens in practice on a large scale as consumers adjust behavior to changing prices on nonessential goods.

Currently, long term interest rates are showing no signs of inflation concern as rates have been falling over the past few months. Even if some inflation seeps through to the economy, the Fed has a tendency to overlook one-time inflationary events where there is direct causation.

Rather than interest rates increase, an escalation in a trade war is more likely to increase demand for Treasuries as a safe haven, thereby pushing yields down. With a global supply chain, tariffs will increase the friction and the cost of goods moving throughout the production process. This could result in slower growth and lower profits for US companies. Again, these are further indications of lower yields.

China does hold $5-6 trillion worth of US Treasury bonds. Investors have long feared that China will use this as a weapon and dump these on the market, causing US rates to jump. Could tariffs be the trigger for such action?

The problem with this logic is that such a move would nuke themselves too. China’s response thus far to the tariffs has been to weaken its currency to help offset the effects of tariffs. The chart below shows the dramatic decline in the Yuan/USD valuation since June. This looks like China trying to offset tariffs with cheaper currency.

Selling Treasury bonds will have the opposite effect. A stronger yuan plus tariffs to their largest trading partner would crush their economy as their exports would become uncompetitive.

From a US standpoint, the economic effects of a trade war are unlikely to push rates higher. This is confirmed by the market’s reaction, or lack thereof. The dollar has remained very strong and long-term rates have fallen.

The real question is if tariffs effect the economy enough to make the Fed change course. At the end of the day, it all circles back to how the Fed and other central banks will respond.

Monday, yields spiked globally as the Bank of Japan mentioned it may raise its interest rate target. Since the financial crisis response of swelling central bank balance sheets, the reality is that they continue to control the rate markets.

The intervention and stimulus on a global scale was unprecedented. This makes forecasting what happens when the accommodation is removed impossible as there is no prior example from which to learn.

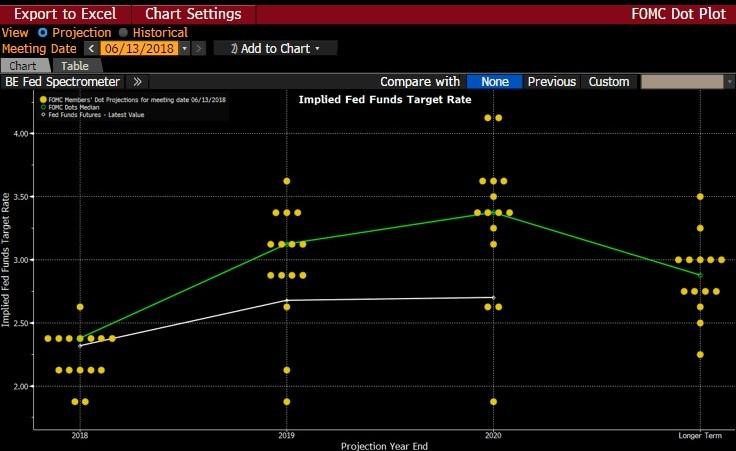

As for the Fed, the market believes it will be forced to slow rate hikes next year. This is illustrated in the nearby chart. The green line shows the Fed’s forecast for fed funds over the coming years. The grey line represents the futures market’s expectation for the path of fed funds.

The Fed expects to continue on the same pace of rate hikes into 2020, with fed funds peaking around 3.5 percent. However, even the Fed acknowledges that it will no longer be accommodative and will be in a tightening posture by the end of 2019 as they forecast the funds rate to be over their long-run expectation of neutral. This means that the Fed is no longer just taking its foot off the gas, but it is beginning to apply the brakes.

The market believes the Fed will only hike three more times and then be forced to stand pat at 2.75 percent. With the 10yr note at 2.95 percent, the market is forecasting a flat yield curve next year, but not believing the Fed will invert the curve. This is a fairly wide deviation in expectations by the market and the Fed.

Does this signal a looming policy error by the Fed? Or is the market anticipating headwinds such as tariffs to force the Fed off course? For the bond market, this looming confrontation between Fed and market expectations is the war to pay attention to, not the battle over tariffs.