Yesterday, I was in the middle of updating a chart about the basic risk and return characteristics of corporate bonds when Standard and Poor’s announced they were downgrading bonds issued by Exxon-Mobile from AAA to AA+.

It’s a shame to see another company lose their prime rating – there are now only two companies that have an AAA-rating. Exxon had held the prime rating since 1930, if you include predecessor entities, and was only the third company to hold the top spot for more than 50 years.

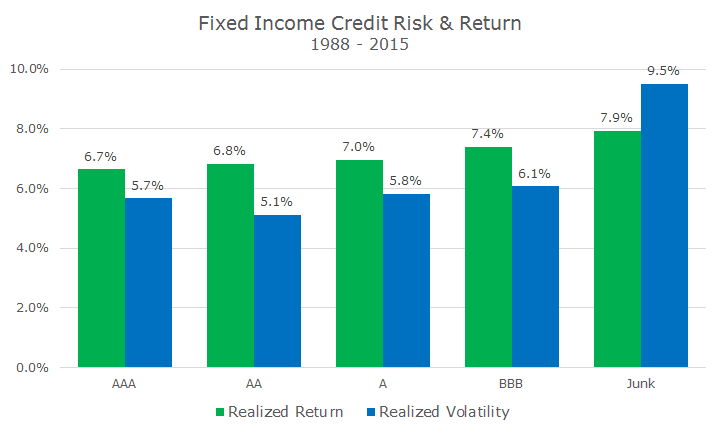

The news helped me interpret the chart below, which contains a small puzzle in my opinion.

The basic idea of the chart is that bonds with more credit risk have earned slightly higher returns (in green) over the long run to compensate investors for the additional risk.

Since we believe that risk and return go hand-in-hand, the chart also shows the realized volatility for each credit rating. In general, the realized volatility increases as well with a particularly sharp spike in non-investment grade, or junk, bonds.

Here’s the puzzle: why does the volatility decrease between AAA and AA bonds? If our theory about risk and return is right, shouldn’t the volatility of AAA bonds be the lowest of the bunch?

I haven’t seen any studies or have an official answer, but I would say that the small number of bonds in the AAA category is probably a big part of the story.

This data, from Barclays, only goes back to 1988 and back then there were still only 60 or some companies that carried the AAA rating. While that’s a lot more than two companies, it makes sense that a more diversified pool of bonds would be less volatile than an un-diversified portfolio.

The other factor to consider is the other main risk of investing in bonds: the term, or duration. Longer term bonds are more volatile than short-term bonds and we don’t know the duration for each of these categories.

Chances are that the duration across all of the categories is similar, but if there are only a few bonds in the AAA group, the duration could be a mismatch.

Despite the quirk in the data, we think the basic risk and return relationship still stands.

The Exxon downgrade also reminded me that even as an AA+, the company has the same rating as the US Treasury.

Recall that in 2011, S&P downgraded the US government to AA+ so there are now two companies that have better credit than the federal government – which is funny because the government has a printing press.

David is a trusted advisor to 50 families, delivering comprehensive financial solutions, including financial planning, investment management, cash management, tax planning, estate planning, and charitable giving. As Chief Investment Officer, he leads the Investment Committee and the research and trading team. His team continuously evaluates investment strategies and securities, working closely with Portfolio Managers to implement them effectively.