The Bureau of Economic Analysis (BEA) released their second estimate of Gross Domestic Product (GDP) yesterday for the first quarter of this year.

Initially, the BEA reported the economy grew by an annualized rate of 0.10 percent, which was a fairly bad print. The cold winter shouldered a lot of the blame, but it also seemed like the economy would have slowed down anyway even if the winter had been more temperate.

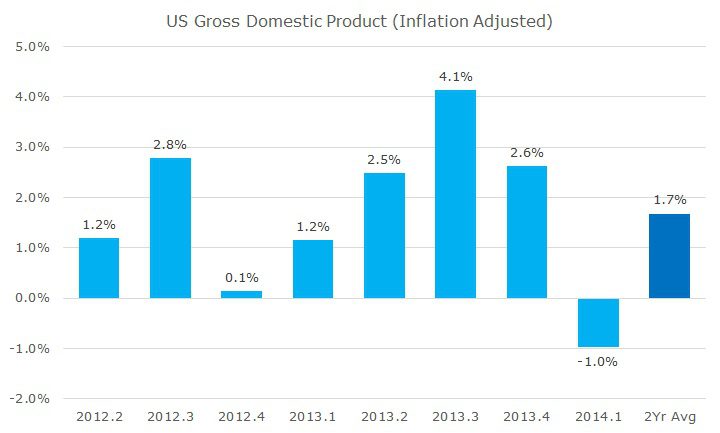

The released yesterday showed that the economy wasn’t just slow, but contracted by an annualized rate of -1.00, which is substantially worse than first reported and what was expected yesterday; the consensus estimate called for -0.50 percent.

The expectation at this point is that since a large part of the contraction can be attributed to the weather, that the economic activity was simply shifted to the second quarter. We’ve got a month left to go before the quarter ends, but economists are busily working on their forecasts, which now call for an annualized real growth rate of 3.5 percent.

Even if you average the realized -1.0 percent and the expected 3.5 percent rate, you only get 1.25 percent for the first half of the year. At the outset of the year, there was a great deal of optimism that growth this year would exceed three percent, which is more in line with the long-term average. It’s hard to imagine at this point how we could possibly achieve the growth necessary to make that happen.

Since the recovery began five years ago, real GDP has only grown by two percent per year and my expectation for 2014 simply suggests more of the same.

While I am negative on the idea of three percent growth rate this year, I don’t think we are looking at a recession at this point.

Although the definition is no longer two consecutive quarters of contraction, two negative prints are a pretty indicator that the folks over at National Bureau of Economic Research (NBER) are likely to do their magic and officially mark recession.

I should also note that while the growth rate is slow, there are some positive fundamental trends. For example, credit appears to be flowing more freely, businesses are profitable, banks are well-capitalized, and even the government’s fiscal situation is better (not great, but better).

Even though the GDP number was negative and worse-than-expected, markets took it in stride: stocks rose and bond prices fell. Ultimately, there was nothing new here: the economy is still sick, but continues to get better.

In the crisis, Warren Buffet said that the economy had the equivalent of a heart attack and needed to be stabilized. When the Federal Reserve cut back on their bond-buying stimulus, I continued his analogy by saying that the doctor was starting to take us off of some of the medicine.

What we have here is simply more of the same.