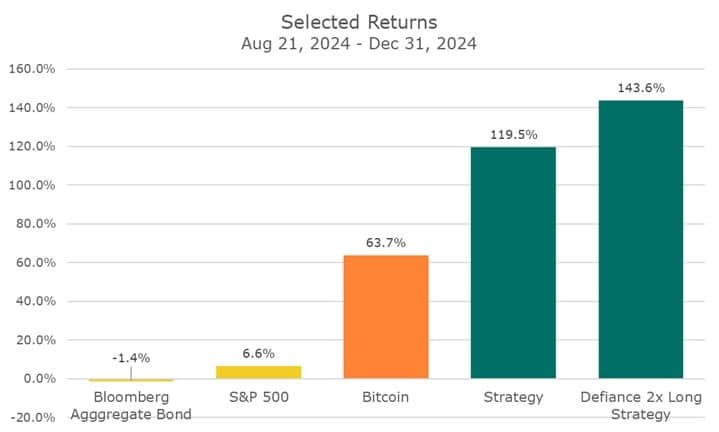

At the 2025 Acropolis Investor Social — a wonderful evening, only to be topped by this year’s Social — I presented the chart below.

The colors were slightly different, and at the time, I hadn’t included the S&P 500 or the Bloomberg Aggregate Bond Index. But the message was clear: pockets of speculative excess were forming in unusual corners of the market.

I began by revealing Bitcoin. Over the final four months of the year, it had risen nearly ten times as much as the stock market. That kind of divergence is a classic signal of froth. The audience groaned — perhaps because the average age in the room wasn’t under 35, or perhaps because few owned Bitcoin.

Next came Strategy (formerly MicroStrategy): a once-unremarkable technology company that effectively converted its balance sheet into Bitcoin and then issued debt to buy more and more Bitcoin. It was up 119.5 percent. What’s a clearer sign of speculative intensity than a company leveraging itself to buy cryptocurrency?

Finally, I showed a leveraged ETF designed to buy two dollars of Strategy for every dollar invested. That, I suggested, was the logical endpoint: an ETF leveraging a leveraged company that itself leverages cryptocurrency. (The next step would presumably be options on the ETF.) Incidentally, the time frame shown happens to match the full life of that ETF.

None of us knew the timing, but there was a shared sense in the room that this couldn’t persist indefinitely. The open question was whether a reversal in Bitcoin and its leveraged cousins would remain contained or spill into the broader equity market.

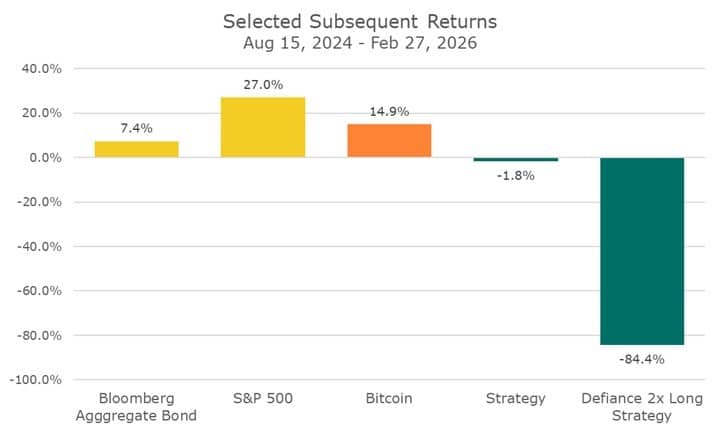

It is still too early to reach firm conclusions. But since year-end 2024, Bitcoin has fallen sharply, down almost a third as the updated chart shows, reflecting cumulative (non-annualized) returns since December 31, 2024. Strategy has fallen by more than half. The leveraged ETF has declined by more than 90 percent.

To be fair, the ETF sponsor, Defiance, is explicit that these products are engineered to deliver two times daily returns, not long-term compounded returns, and are intended primarily for traders. That structural reality explains much of the damage, though it does not change the lesson. (Morningstar has a useful discussion of this dynamic.)

When we combine the surge and the collapse, the full-period picture is instructive. Bitcoin ultimately underperformed the S&P 500, though it outpaced bonds. Strategy ended up roughly flat. Long-term holders of the leveraged ETF were effectively destroyed.

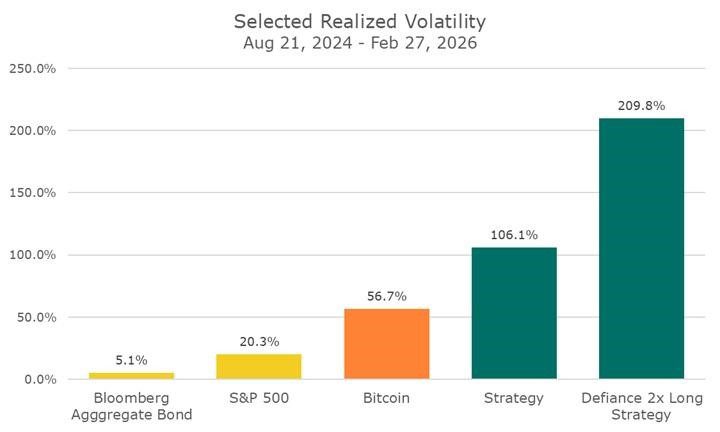

Volatility tells the same story. You do not need a statistics background to interpret the chart. Over this period (and generally) equities are roughly four times as volatile as bonds. Bitcoin was more than twice as volatile as the S&P 500. Strategy was about twice as volatile as Bitcoin. The leveraged ETF was roughly twice as volatile as Strategy. Who knows what the options would be?

I once heard Eugene Fama, the Nobel Prize–winning pioneer of modern finance, say something like: “A standard deviation over 50 basically tells you you’ll be wiped out in 20 years.”

That’s enough to keep me away from Bitcoin. As for Strategy, I’ll leave that to others. And the leveraged ETF, for practical purposes, has already demonstrated the point.

As an interesting aside, Defiance also launched a 2x ETF that shorts Strategy. It is down 96.4 percent over the same period. That symmetry reinforces the conclusion: leveraged ETFs, whether long or short, are extraordinarily unforgiving vehicles.

The broader lesson is straightforward. Risky strategies can produce dramatic outcomes, both up and down. The determining factor for an investor is often not security selection, but their position size.

For now, my own position size in Bitcoin remains zero, though I’m open to the possibility that I could be wrong. Some clients hold modest allocations, and that’s okay. Their experience has been volatile and uncomfortable of late, but because the position sizes were appropriate, the drawdowns have not been destabilizing.

As I get older, I find myself returning to a principle I was told early in my career: position sizing is as important as security selection. At the time, I focused almost exclusively on picking the right securities. To paraphrase George Bernard Shaw, education is often wasted on the young.

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott

- David Ott